【数学建模】基于matlab时变参数随机波动率向量自回归模型(TVP-VAR)【含Matlab源码 037期】

【摘要】

一、获取代码方式

获取代码方式1: 完整代码已上传我的资源:【数学建模】基于matlab时变参数随机波动率向量自回归模型(TVP-VAR)【含Matlab源码 037期】

获取代码方式2: 通过订阅紫...

一、获取代码方式

获取代码方式1:

完整代码已上传我的资源:【数学建模】基于matlab时变参数随机波动率向量自回归模型(TVP-VAR)【含Matlab源码 037期】

获取代码方式2:

通过订阅紫极神光博客付费专栏,凭支付凭证,私信博主,可获得此代码。

备注:

订阅紫极神光博客付费专栏,可免费获得1份代码(有效期为订阅日起,三天内有效);

二、部分源代码

%==================================4.1 Main================================

clear;

clc;

% Load Korobilis (2008) quarterly data

load ydata.dat; % data

load yearlab.dat; % data labels

%%

%----------------------------------BASICS----------------------------------

Y=ydata;

t=size(Y,1); % t - The total number of periods in the raw data (t=215)

M=size(Y,2); % M - The dimensionality of Y (i.e. the number of variables)(M=3)

tau = 40; % tau - the size of the training sample (the first forty quarters)

p = 2; % p - number of lags in the VAR model

%% Generate the Z_t matrix, i.e. the regressors in the model.

ylag = mlag2(Y,p); % This function generates a 215x6 matrix with p lags of variable Y.

ylag = ylag(p+tau+1:t,:); % Then remove our training sample, so now a 173x6 matrix.

K = M + p*(M^2); % K is the number of elements in the state vector

% Here we distribute the lagged y data into the Z matrix so it is

% conformable with a beta_t matrix of coefficients.

Z = zeros((t-tau-p)*M,K);

for i = 1:t-tau-p

ztemp = eye(M);

for j = 1:p

xtemp = ylag(i,(j-1)*M+1:j*M);

xtemp = kron(eye(M),xtemp);

ztemp = [ztemp xtemp];

end

Z((i-1)*M+1:i*M,:) = ztemp;

end

% Redefine our variables to exclude the training sample and the first two

% lags that we take as given, taking total number of periods (t) from 215

% to 173.

y = Y(tau+p+1:t,:)';

yearlab = yearlab(tau+p+1:t);

t=size(y,2); % t now equals 173

%% --------------------MODEL AND GIBBS PRELIMINARIES-----------------------

nrep = 5000; % Number of sample draws

nburn = 2000; % Number of burn-in-draws

it_print = 100; % Print in the screen every "it_print"-th iteration

%% INITIAL STATE VECTOR PRIOR

% We use the first 40 observations (tau) to run a standard OLS of the

% measurement equation, using the function ts_prior. The result is

% estimates for priors for B_0 and Var(B_0).

[B_OLS,VB_OLS]= ts_prior(Y,tau,M,p);

% Given the distributions we have, we now have to define our priors for B,

% Q and Sigma. These are set in accordance with how they are set in

% Primiceri (2005). These are the hyperparameters of the beta, Q and Sigma

% initial priors.

B_0_prmean = B_OLS;

B_0_prvar = 4*VB_OLS;

Q_prmean = ((0.01).^2)*tau*VB_OLS;

Q_prvar = tau;

Sigma_prmean = eye(M);

Sigma_prvar = M+1;

% To start the Kalman filtering assign arbitrary values that are in support

% of their priors, Q and Sigma.

consQ = 0.0001;

Qdraw = consQ*eye(K);

Sigmadraw = 0.1*eye(M);

% Create some matrices for storage that will be filled in once we

% start the Gibbs sampling.

Btdraw = zeros(K,t);

Bt_postmean = zeros(K,t);

Qmean = zeros(K,K);

Sigmamean = zeros(M,M);

%% -------------------------IRF-PRELIMINARIES------------------------------

nhor = 21; % The number of periods in the impulse response function.

% Matricies to be filled containing IRFs for 1975q1, 1981q3, 1996q1. The

% dimensions correspond to the iterations of the gibbs sample, each of the

% variables, and each of the 21 periods of the IRF analysis.

imp75 = zeros(nrep,M,nhor);

imp81 = zeros(nrep,M,nhor);

imp96 = zeros(nrep,M,nhor);

% This corresponds to variable J introduced in equation (14) in the report

bigj = zeros(M,M*p);

bigj(1:M,1:M) = eye(M);

%% ================ START GIBBS SAMPLING ==================================

tic; % This is just a timer

disp('Number of iterations');

for irep = 1:nrep + nburn % 7000 gibbs iterations starts here

% Print iterations - this just updates on the progress of the sampling

if mod(irep,it_print) == 0

disp(irep);toc;

end

%% Draw 1: B_t from p(B_t|y,Sigma)

% We use the function 'carter_kohn_hom' to to run the FFBS algorithm.

% This results in a 21x173 matrix, corresponding to one Gibbs sample

% draw of each of the coefficients in each time period. The inputs

% Sigmadraw and Qdraw are updated for each Gibbs sample repetition.

[Btdraw] = carter_kohn_hom(y,Z,Sigmadraw,Qdraw,K,M,t,B_0_prmean,B_0_prvar);

%% Draw 2: Q from p(Q^{-1}|y,B_t) which is i-Wishart

% We draw Q from an Inverse Wishart distribution. The parameters

% of the distribution are derived as equation (11) in the main report.

% The mean is taken as the inverse of the accumulated sum of squared

% errors added to the prior mean, and the variance is simply t.

% Differencing Btdraw to create the sum of squared errors

Btemp = Btdraw(:,2:t)' - Btdraw(:,1:t-1)';

sse_2Q = zeros(K,K);

for i = 1:t-1

sse_2Q = sse_2Q + Btemp(i,:)'*Btemp(i,:);

end

Qinv = inv(sse_2Q + Q_prmean); % compute mean to use for Wishart draw

Qinvdraw = wish(Qinv,t+Q_prvar); % draw inv q from the wishart distribution

Qdraw = inv(Qinvdraw); % find non-inverse q

%% Draw 3: Sigma from p(Sigma|y,B_t) which is i-Wishart

% We draw Sigma from an Inverse Wishart distribution. The parameters

% of the distirbution are derived as equation (10) in the main report.

% The mean is taken as the inverse of the sum of squared residuals

% added to the prior mean. The variance is simply t.

% Find residuals using data and the current draw of coefficients

resids = zeros(M,t);

for i = 1:t

resids(:,i) = y(:,i) - Z((i-1)*M+1:i*M,:)*Btdraw(:,i);

end

% Create a matrix for the accumulated sum of squared residuals, to

% be used as the mean parameter in the i-Wishart draw below.

sse_2S = zeros(M,M);

for i = 1:t

sse_2S = sse_2S + resids(:,i)*resids(:,i)';

end

Sigmainv = inv(sse_2S + Sigma_prmean); % compute mean to use for the Wishart

Sigmainvdraw = wish(Sigmainv,t+Sigma_prvar); % draw from the Wishsart distribution

Sigmadraw = inv(Sigmainvdraw); % turn into non-inverse Sigma

%% IRF

% We only apply IRF analysis once we have exceeded the burn-in draws phase.

if irep > nburn;

% Create matrix that is going to contain all beta draws over

% which we will take the mean after the Gibbs sampler as our moment

% estimate:

Bt_postmean = Bt_postmean + Btdraw;

% biga is the A matrix of the VAR(1) version of our VAR(2) model,

% found in equation (12. biga changes in every period of the

% analysis, because the coefficients are time varying, so we

% apply the analysis below in every time period.

biga = zeros(M*p,M*p);

for j = 1:p-1

biga(j*M+1:M*(j+1),M*(j-1)+1:j*M) = eye(M); % fill the A matrix with identity matrix (3) in bottom left corner

end

% The following procedure is applied separately in each time period.

% This loop takes coefficients of the relevant time period from

% Bt_draw (which contains all coefficients for all t) and uses

% them to update the biga matrix, so that it can change for

% every t.

for i = 1:t

bbtemp = Btdraw(M+1:K,i); % get the draw of B(t) at time i=1,...,T (exclude intercept)

splace = 0;

for ii = 1:p

for iii = 1:M

biga(iii,(ii-1)*M+1:ii*M) = bbtemp(splace+1:splace+M,1)'; % Load non-intercept coefficient draws

splace = splace + M;

end

end

% Next we want to create a shock matrix in which the third

% column is [0 0 1]', therefore implementing a unit shock

% in the interest rate.

shock = eye(3);

% Now get impulse responses for 1 through nhor future

% periods. impresp is a 3x63 matrix which contains 9

% response values in total for each period, 3 for each

% variable. These three responses correspond to the 3

% possible shocks that are contained in the schock

% matrix

% bigai is updated through mulitiplication with the

% coefficient matrix after each time period.

% Create a results matrix to store impulse responses in all periods

impresp = zeros(M,M*nhor);

% Fill in the first period of the results matrix with the shock (as defined above)

impresp(1:M,1:M) = shock;

% Create a separate variable for the a matrix so that we

% can update it for each period of the IRF analysis.

bigai = biga;

% This follows the impulse response function as in equation 15.

% Fill in each period of the results matrix according to

% the impulse response function formula.

for j = 1:nhor-1

impresp(:,j*M+1:(j+1)*M) = bigj*bigai*bigj'*shock;

bigai = bigai*biga; % update the coefficient matrix for next period

end

% The section below keeps only the responses that we are interested in:

% - those from the periods 1975q1, 1981q3, and 1996q1

% - those that correspond to the shock in the interest

% rate (i.e. those caused by the third column of our shock

% matrix).

if yearlab(i,1) == 1975.00; % store only IRF from 1975:Q1

impf_m = zeros(M,nhor);

jj=0;

for ij = 1:nhor

jj = jj + M; % select only the third column for each time period of the IRF

impf_m(:,ij) = impresp(:,jj);

end

% For each iteration of the Gibbs sampler, fill in the

% results along the first dimension

imp75(irep-nburn,:,:) = impf_m;

end

if yearlab(i,1) == 1981.50; % store only IRF from 1981:Q3

impf_m = zeros(M,nhor);

jj=0;

for ij = 1:nhor

jj = jj + M; % select only the third column for each time period of the IRF

impf_m(:,ij) = impresp(:,jj);

end

% For each iteration of the Gibbs sample, fill in the

% results along the first dimension

imp81(irep-nburn,:,:) = impf_m;

end

if yearlab(i,1) == 1996.00; % store only IRF from 1996:Q1

impf_m = zeros(M,nhor);

jj=0;

for ij = 1:nhor

jj = jj + M; % select only the third column for each time period of the IRF

impf_m(:,ij) = impresp(:,jj);

end

% For each iteration of the Gibbs sample, fill in the

% results along the first dimension

imp96(irep-nburn,:,:) = impf_m;

end

end % End getting impulses for each time period

end % End the impulse response calculation section

end % End main Gibbs loop (for irep = 1:nrep+nburn)

clc;

toc; % Stop timer and print total time

%% ================ END GIBBS SAMPLING ==================================

% Even though it is not used in our IRF analysis since we are integrating

% that into the Gibbs sampling loop, here is how to take the mean of the

% draw of the betas as moment estimate:

Bt_postmean = Bt_postmean./nrep;

%% Graphs and tables

% This works out the percentage range of that each variable's coefficient

% spans across time. I.e. to what extent was the TVP facility used by each

% variable in the model? This is calculated by finding the range for each

% variable as a percentage of the mean coefficient size for that variable.

% The result is a 21x1 vector, and it is reshaped into a 3x7 matrix in order

% to map onto the system of equations (2,3,and 4) set out in the report.

Bt_range = ones(21,1)

for i = 1:21

Bt_range(i) = abs((max(Bt_postmean(i,:))-min(Bt_postmean(i,:)))/mean(Bt_postmean(i,:)))

end

Bt_range = reshape(Bt_range,3,7)

% Create a table of coefficient ranges for export to the report

rowNames = {'Inflation','Unemployment','Interest Rate'};

colNames = {'Intercept','Inf_1','Unemp_1', 'IR_1','Inf_2','Unemp_2', 'IR_2'};

pc_change_table = array2table(Bt_range,'RowNames',rowNames,'VariableNames',colNames)

writetable(pc_change_table,'pc_change.csv')

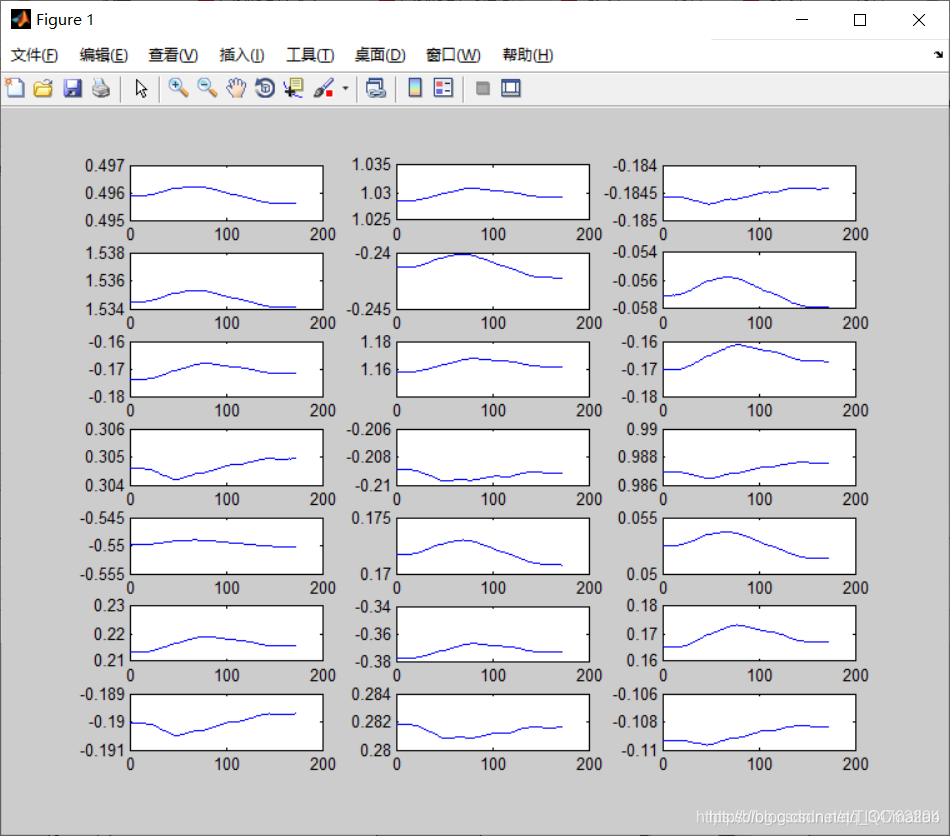

% Now plot a separate chart for each of the coefficients

figure

for i = 1:21

subplot(7,3,i)

plot(1:t,Bt_postmean(i,:))

end

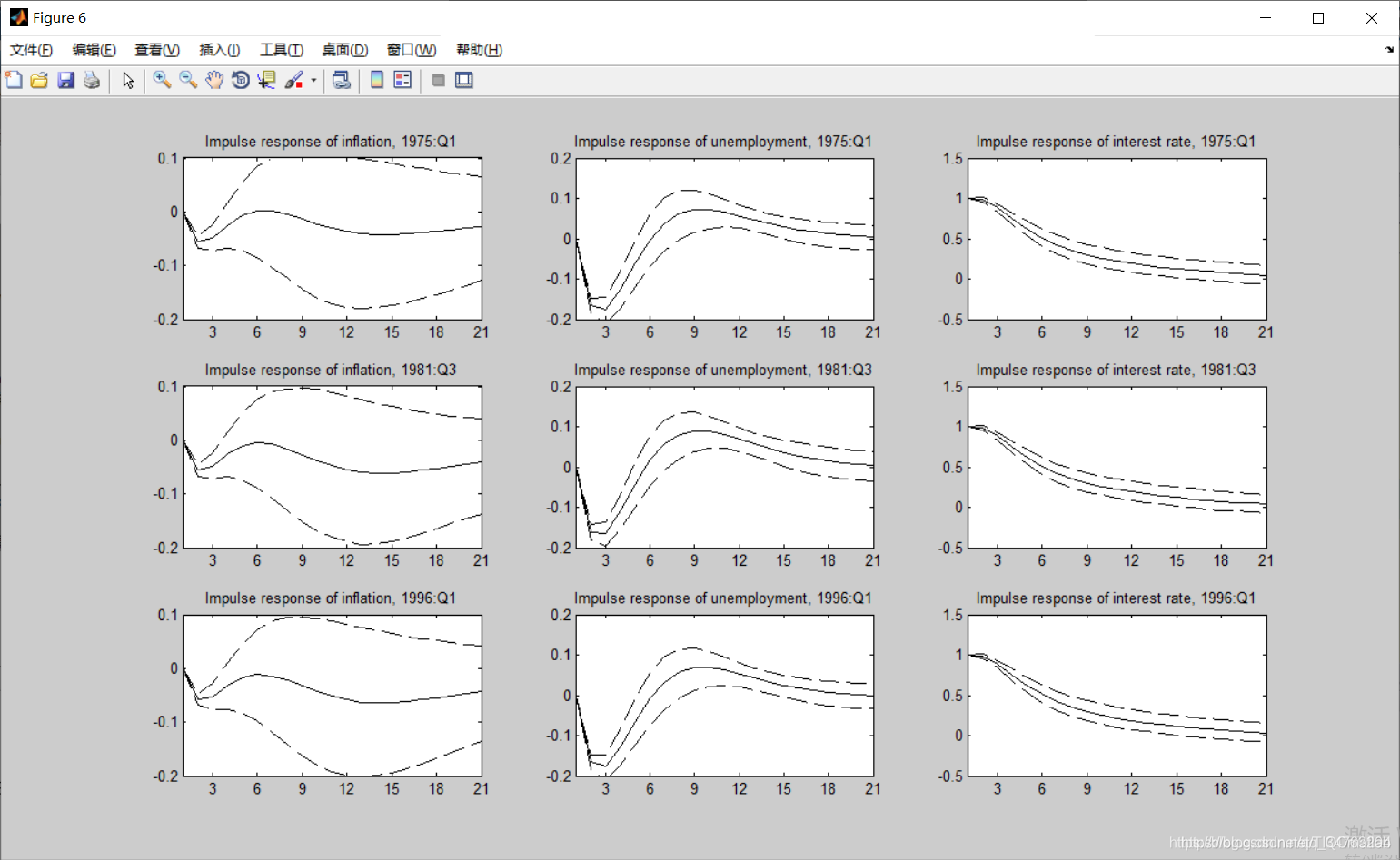

% Now we move to plotting the IRF. This section takes moments along the

% first dimension, i.e. across the Gibbs sample iterations. The moments

% are for the 16th, 50th and 84th percentile.

qus = [.16, .5, .84];

imp75XY=squeeze(quantile(imp75,qus));

imp81XY=squeeze(quantile(imp81,qus));

imp96XY=squeeze(quantile(imp96,qus));

% Plot impulse responses

figure

set(0,'DefaultAxesColorOrder',[0 0 0],...

'DefaultAxesLineStyleOrder','--|-|--')

subplot(3,3,1)

plot(1:nhor,squeeze(imp75XY(:,1,:)))

title('Impulse response of inflation, 1975:Q1')

xlim([1 nhor])

ylim([-0.2 0.1])

% % yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,2)

plot(1:nhor,squeeze(imp75XY(:,2,:)))

title('Impulse response of unemployment, 1975:Q1')

xlim([1 nhor])

ylim([-0.2 0.2])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,3)

%ylim([0 1])

% % yline(0)

plot(1:nhor,squeeze(imp75XY(:,3,:)))

title('Impulse response of interest rate, 1975:Q1')

xlim([1 nhor])

%ylim([-0.3 0.1])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,4)

plot(1:nhor,squeeze(imp81XY(:,1,:)))

title('Impulse response of inflation, 1981:Q3')

xlim([1 nhor])

ylim([-0.2 0.1])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,5)

plot(1:nhor,squeeze(imp81XY(:,2,:)))

title('Impulse response of unemployment, 1981:Q3')

xlim([1 nhor])

ylim([-0.2 0.2])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,6)

plot(1:nhor,squeeze(imp81XY(:,3,:)))

title('Impulse response of interest rate, 1981:Q3')

xlim([1 nhor])

%ylim([-0.4 0.1])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,7)

plot(1:nhor,squeeze(imp96XY(:,1,:)))

title('Impulse response of inflation, 1996:Q1')

xlim([1 nhor])

ylim([-0.2 0.1])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,8)

plot(1:nhor,squeeze(imp96XY(:,2,:)))

title('Impulse response of unemployment, 1996:Q1')

xlim([1 nhor])

ylim([-0.2 0.2])

% yline(0)

set(gca,'XTick',0:3:nhor)

subplot(3,3,9)

plot(1:nhor,squeeze(imp96XY(:,3,:)))

title('Impulse response of interest rate, 1996:Q1')

xlim([1 nhor])

%ylim([0 1])

% yline(0)

set(gca,'XTick',0:3:nhor)

disp(' ')

disp('To plot impulse responses, use: plot(1:nhor,squeeze(imp75XY(:,VAR,:))) ')

disp(' ')

disp('where VAR=1 for impulses of inflation, VAR=2 for unemployment and VAR=3 for interest rate')

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25

- 26

- 27

- 28

- 29

- 30

- 31

- 32

- 33

- 34

- 35

- 36

- 37

- 38

- 39

- 40

- 41

- 42

- 43

- 44

- 45

- 46

- 47

- 48

- 49

- 50

- 51

- 52

- 53

- 54

- 55

- 56

- 57

- 58

- 59

- 60

- 61

- 62

- 63

- 64

- 65

- 66

- 67

- 68

- 69

- 70

- 71

- 72

- 73

- 74

- 75

- 76

- 77

- 78

- 79

- 80

- 81

- 82

- 83

- 84

- 85

- 86

- 87

- 88

- 89

- 90

- 91

- 92

- 93

- 94

- 95

- 96

- 97

- 98

- 99

- 100

- 101

- 102

- 103

- 104

- 105

- 106

- 107

- 108

- 109

- 110

- 111

- 112

- 113

- 114

- 115

- 116

- 117

- 118

- 119

- 120

- 121

- 122

- 123

- 124

- 125

- 126

- 127

- 128

- 129

- 130

- 131

- 132

- 133

- 134

- 135

- 136

- 137

- 138

- 139

- 140

- 141

- 142

- 143

- 144

- 145

- 146

- 147

- 148

- 149

- 150

- 151

- 152

- 153

- 154

- 155

- 156

- 157

- 158

- 159

- 160

- 161

- 162

- 163

- 164

- 165

- 166

- 167

- 168

- 169

- 170

- 171

- 172

- 173

- 174

- 175

- 176

- 177

- 178

- 179

- 180

- 181

- 182

- 183

- 184

- 185

- 186

- 187

- 188

- 189

- 190

- 191

- 192

- 193

- 194

- 195

- 196

- 197

- 198

- 199

- 200

- 201

- 202

- 203

- 204

- 205

- 206

- 207

- 208

- 209

- 210

- 211

- 212

- 213

- 214

- 215

- 216

- 217

- 218

- 219

- 220

- 221

- 222

- 223

- 224

- 225

- 226

- 227

- 228

- 229

- 230

- 231

- 232

- 233

- 234

- 235

- 236

- 237

- 238

- 239

- 240

- 241

- 242

- 243

- 244

- 245

- 246

- 247

- 248

- 249

- 250

- 251

- 252

- 253

- 254

- 255

- 256

- 257

- 258

- 259

- 260

- 261

- 262

- 263

- 264

- 265

- 266

- 267

- 268

- 269

- 270

- 271

- 272

- 273

- 274

- 275

- 276

- 277

- 278

- 279

- 280

- 281

- 282

- 283

- 284

- 285

- 286

- 287

- 288

- 289

- 290

- 291

- 292

- 293

- 294

- 295

- 296

- 297

- 298

- 299

- 300

- 301

- 302

- 303

- 304

- 305

- 306

- 307

- 308

- 309

- 310

- 311

- 312

- 313

- 314

- 315

- 316

- 317

- 318

- 319

- 320

- 321

- 322

- 323

- 324

- 325

- 326

- 327

- 328

- 329

- 330

- 331

- 332

- 333

- 334

- 335

- 336

- 337

- 338

- 339

- 340

- 341

- 342

- 343

- 344

- 345

- 346

- 347

- 348

- 349

- 350

- 351

- 352

- 353

- 354

- 355

- 356

- 357

- 358

- 359

- 360

- 361

- 362

- 363

- 364

- 365

- 366

- 367

- 368

- 369

- 370

- 371

- 372

- 373

- 374

- 375

- 376

- 377

- 378

- 379

- 380

- 381

- 382

- 383

- 384

- 385

- 386

- 387

- 388

- 389

- 390

- 391

- 392

- 393

- 394

- 395

- 396

- 397

- 398

- 399

- 400

- 401

- 402

- 403

- 404

- 405

- 406

- 407

- 408

- 409

- 410

- 411

- 412

- 413

- 414

三、运行结果

四、matlab版本及参考文献

1 matlab版本

2014a

2 参考文献

[1]李昕.MATLAB数学建模[M].清华大学出版社.2017

[2]王健,赵国生.MATLAB数学建模与仿真[M].清华大学出版社.2016

[3]余胜威.MATLAB数学建模经典案例实战[M].清华大学出版社.2015

文章来源: qq912100926.blog.csdn.net,作者:海神之光,版权归原作者所有,如需转载,请联系作者。

原文链接:qq912100926.blog.csdn.net/article/details/112152864

【版权声明】本文为华为云社区用户转载文章,如果您发现本社区中有涉嫌抄袭的内容,欢迎发送邮件进行举报,并提供相关证据,一经查实,本社区将立刻删除涉嫌侵权内容,举报邮箱:

cloudbbs@huaweicloud.com

- 点赞

- 收藏

- 关注作者

评论(0)